From the lows of the Financial Crisis of 2008, the U.S. stock market has rebounded well over 400%. GDP, however, has averaged roughly 2% growth during the years leading up to the coronavirus pandemic. Many investors question why the market has rallied exponentially more than the economy has grown? The answer is T.I.N.A. – There Is No Alternative!

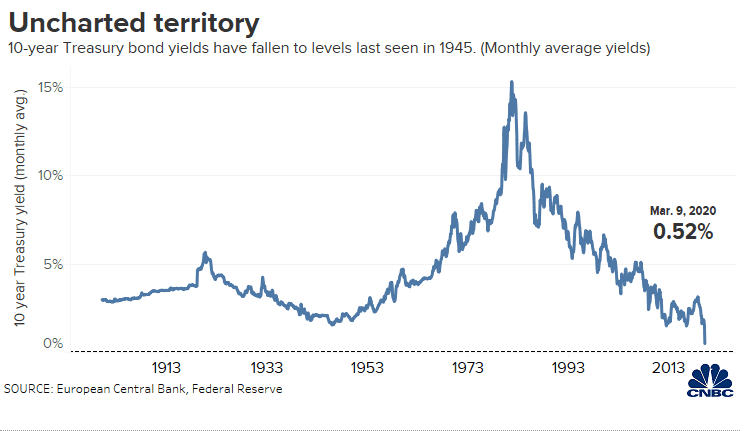

In order to inject money into the banking system to spur lending, prop up the beleaguered housing market, and increase employment, the Federal Reserve initiated their Quantitative Easing (QE) program. The purchase of Treasury securities by the Fed from banks increased the money supply, adding liquidity to financial system, and lowered interest rates due to the added demand. The first rounds of QE ended in 2014. However, the coronavirus crisis in 2020 prompted the Fed to reestablish their Treasury purchases. And this active participation in the Treasury markets by the Fed has kept interest rates at historically low levels.

Investors require return. When a security offers little to no return, investors will seek it elsewhere. This simplified truth has fueled the stock market, through the pandemic, as the return on bonds (the yield) have remained exceptionally low.

With the continued decline in yields, investors chasing higher returns have accelerated the flow of money into equities. The market has defied the global financial impacts and struggles caused by the pandemic. For individual and institutional portfolio managers there is no alternative to stocks as long as interest rates remain subdued by the Fed.

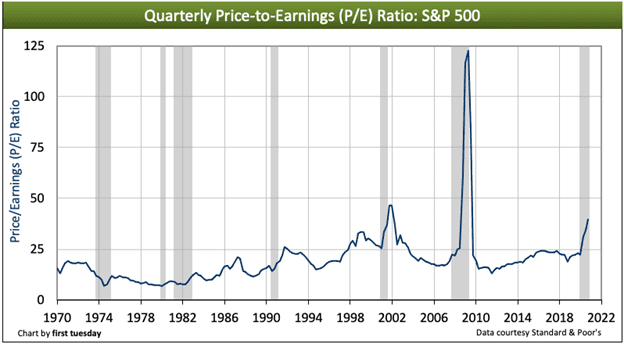

Despite this extended period of low rates, the U.S. economy has had only moderate growth and low inflation. Yet the stock market has soared to new highs. While some companies have thrived in the new WFH economy, many have not. It is T.I.N.A. that fuels the market surge: portfolio managers continue to chase return while 401k money constantly needs to be invested. This has led to overstretched valuations, as measured by the Price-to-Earnings ratio (P/E) of the S&P 500 Index.

The P/E ratio has two components, price and earnings per share. For the S&P 500 Index, the P/E ratio is the price of the Index divided by the aggregate earnings per share of the entire 500 stocks that make up the index. As with any ratio, the number rises if either the price goes higher, or the earnings drops.

The last two times the P/E ratio of the S&P 500 Index were at extreme levels occurred during the 2001 Dot-Com Bubble and the 2008 Financial Crisis. In both instances the P/E levels skyrocketed as the earnings denominator collapsed. Now in 2021, while earnings have been impacted by the pandemic, they remain stable overall.

The Index, however, has risen impressively, thereby lifting the P/E ratio to the current extended valuation. Thank you T.I.N.A.! Unless the economy improves dramatically and creates higher earnings growth, a normalization of price is inevitable.

The Federal Reserve is basically concerned with two financial conditions: inflation and employment. The current focus is employment as the economy attempts to recover from the pandemic setbacks. Fed Chairman Jerome Powell has stated that ultralow interest rates will be maintained until maximum employment is achieved and inflation hits 2% (currently 1.4%). This consistent message has kept short-term interest rates near zero. However, unfortunately for T.I.N.A., there are four factors that may force rates higher:

These forces have combined to increase investor expectations of interest rate upward bias. While the actual increase has so far been modest, the fear of a continued upward pull in rates creates investor uncertainty. And uncertainty makes the stock market nervous.

In Summary

The T.I.N.A. market has been remarkable, overcoming an abundance of potentially catastrophic influences: trade wars, a divisive election and antagonistic politics, and the unforeseen and tragic pandemic. None of these have had a lasting negative effect. And the Federal Reserve’s mandate to maintain historically low interest rates to promote job creation is the reason. However, markets are cyclical. This low-rate cycle – and the byproduct T.I.N.A. market surge – may be in jeopardy. And despite the Fed’s continued efforts, T.I.N.A. may not survive.

Wealthplicity Recent Posts