The Fed and the bond market are telling investors that interest rates will be lower after inflation subsides, approximately within two years. The Fed believes that an eventual resolution to the war in Ukraine and its energy price impact, a gradual diminishing of supply-chain logjams, and the impact of their increase in short-term rates to temper the demand side of increasing costs will all result in bringing inflation under control. The bond market – utilizing the Fed Funds futures market as a proxy for expectations – sees the Fed Fund peaking possibly near 3% by September of 2023 and then dropping to 2% by 2025. Thus, the Fed and institutional market participants both see interest rates declining after approximately eighteen months. However, investors should be aware that there is an external market force outside the Fed’s control that may fuel higher rates for longer than expected: the deterioration of the U.S. Dollar as the global reserve currency.

Russia’s unprovoked invasion of Ukraine has resulted in coordinated economic sanctions by predominantly NATO bloc countries, led by the United States. The Biden administration has sponsored a major curtailment of Russian companies, financial institutions, and uber-wealthy oligarchs from the global economy. A number of Russian banks (but not all) have been cut off from SWIFT (Society for Worldwide Interbank Financial Communication) which provides a secure messaging system that connects over 11,000 financial institutions in more than 200 countries to enable cross-border payments.

While no payments are made over SWIFT, it contains messages with secure and reliable information directing where, when, and how money is sent between financial entities. SWIFT has become vital to international trade and money flows. As a senior White House official stated last month, “most banks around the world will simply stop transacting with Russian banks that are removed from SWIFT.” As a result, while greatly hampering Russia’s ability to financially interact with the West in the hopes that it would force the termination of hostilities, it has prompted a move by Russia away from Western, Dollar-dominated financial systems and towards a stronger economic reliance upon China. Many other countries, either neutral or anti-U.S./West, have observed the effect of these economic sanctions and will seek to limit them from materially impact them if they run afoul of U.S. or Western European policies.

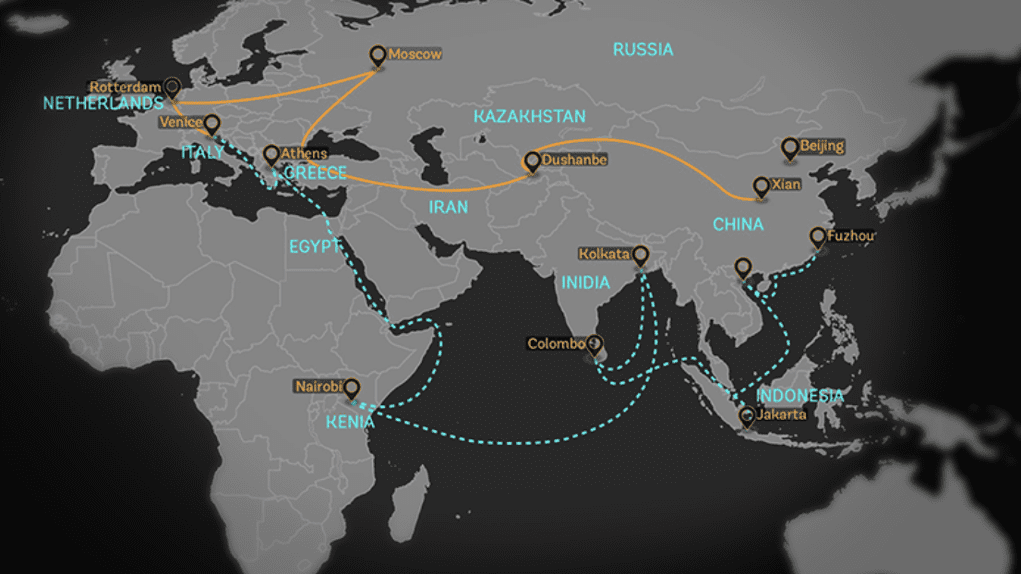

Nor has China been sitting strategically idle, complacently allowing market forces to determine outcomes. During this past decade of Xi Jinping’s reign, China has implemented its “Belt and Road Initiative” (BRI). This attempt to revitalize the ancient Silk Road trade routes employs a land-based Economic Belt plus a Maritime Silk Road, utilizing direct foreign investment to establish favorable economic and military alliances and cooperation.

The BRI, concurrent with a fast growing and technologically advanced Chinese Navy created to diminish US oversight of maritime trade, has established and strengthened economic relationships with anti-US/Western nations and countries that desire reduced reliance upon Western markets and governments. Besides Russia, these countries are throughout highly populated and mineral-rich Southeast Asia (including India), the Middle East and Africa.

More recently, the Chinese central bank has launched both the digital yuan (e-CNY) and the Petroyuan. They are the first major economy to authorize a central bank sponsored blockchain based currency. This places China at the forefront of the evolving migration away from paper currency. Utilizing the transactional components of current cryptocurrencies without their inherent decentralized deficiencies, such as volatility and lack of government control (see Can Cryptocurrency Actually Become a Real Currency), China has established the blueprint for a crypto-like fiat currency. It will serve as both digital payment system, competing against popular Alipay and WeChat pay, but also as a means of transaction without the internet, providing greater cross-platform flexibility.

The beta version was launched within the past two years and now has over 260 million individual users in over 20 cities. While this represents just over 18% of the population, it provides credibility to the international community as to its viability. And poses a risk to the United States. As a recent Asia Fund Managers report noted, “If China decides to settle (cross-border) trade using the digital yuan, it won’t need (its) hefty USD reserves and will be shielded from any potential sanctions from Washington.”

Another new Chinese monetary phenomenon is the Petroyuan, developed to compete with Petrodollars. The term Petrodollar was coined in the 1970s as the US dollar became the universally accepted medium for buying and selling oil, as well as other commodities, among international traders and nations. After World War II, oil demand has grown steadily, in pace with global industrialization. So too did the need for nations to hold an increasing amount of U.S. currency in reserves to purchase the necessary oil. As oil fueled the world’s economic growth, it was the U.S. dollar that kept it flowing.

However, in March of 2018, the first trades in crude oil denominated in yuan occurred on the Shanghai Exchange, and since March of this year, China and Saudi Arabia have been in talks to price some of its oil in Petroyuans. The United States currently imports roughly only 25% of the volume of Middle Eastern oil that it demanded in the 1970s. However, as China has become the world’s largest importer, there is a natural pull away from Petrodollars. The Petrodollar has been the unifying currency for international oil trading and ultimately the significant majority of global trade. Any weakness in this hegemony threatens the U.S. dollar’s and dollar denominated securities’ positions as ”must haves” by foreign countries for economic growth. And, as the Oxford Institute for Energy Studies notes, “Beijing … aim(s) to challenge the U.S. dollar’s dominance as a global reserve currency.”

While few pundits foresee a rapid rise to prominence of the Petroyuan, the current sanctions on Russia, plus the ongoing sanctions against another energy-heavy regime in Iran, have opened the gate wider for those countries antagonistic (Venezuela, Brazil) or not aligned (India, Indonesia) with the U.S.to seek an alternative to Petrodollars to circumvent any chance of restrictions on trade or finance. As former IMF, Federal Reserve and World Bank economist Nouriel Roubini concluded in the Guardian in 2020, “while the dollar’s position is safe for now, it faces significant challenges in the years and decades ahead…the Chinese model has already become quite attractive to many emerging markets and less democratic countries. Over time, as China’s economic, financial, technological, and geopolitical power expands, its currency may make inroads in many more parts of the world.” This reverse globalization inherently reduces the world’s dependence upon the U.S. dollar.

Another major factor impacting the global outlook on dollar denominated securities is inflation. Skyrocketing price pressures, especially in the United States, reduces the attractiveness to other countries of holding our government bonds. As the Fed raises rates in an attempt to contain inflation, all government bonds previously issued lose value. In an extended zero/low-rate environment there is no negative impact to own U.S. debt securities. However, during rising rates, lower interest rate bonds are less attractive to other investors and require discounted prices to create buyer demand. With persistent inflation, foreign entities have declining incentives to maintain U.S. dollar-backed debt. All these factors – the war in Ukraine, Chinese monetary strategies, receding globalization, and inflation – threaten the U.S. dollar’s status as the global reserve currency.

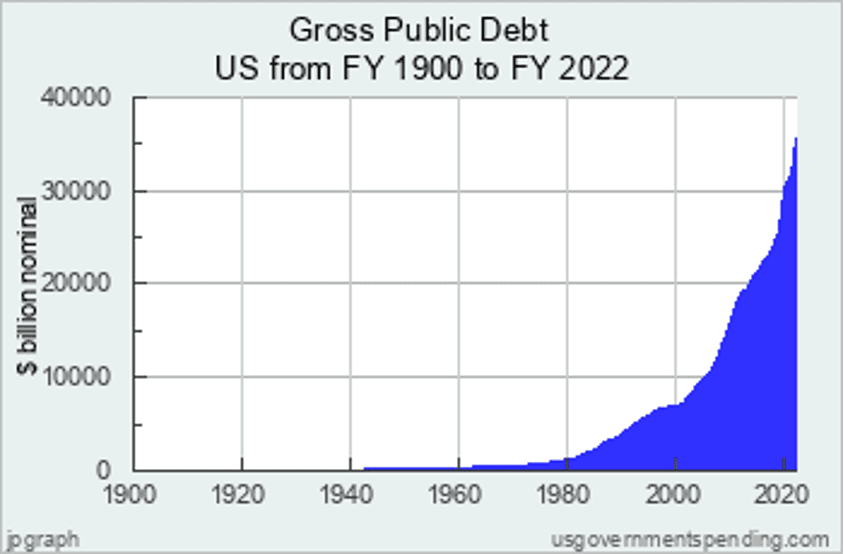

Since going off the gold standard in 1971, which had pegged the value of a dollar to a specific value of gold, the United States government – unshackled by any amount of gold reserves held – has been able to issue greater amounts of debt. This has allowed the government to spend their way out of fiscal problems and crises while substantially increasing the federal deficit.

Once the United States dollar achieved global reserve currency status other nations have been forced to hold dollar-denominated debt securities in order to fuel international trade and economic growth. Basically, the rest of the world has been financing our free spending, and because of their demand for our bonds as dollar reserves – to purchase oil, to purchase other imported goods and services, and to enable international trade – we are able to maintain (sans inflation) lower rates in the U.S. And these lower rates have fueled our own financial strength and the ability to weather well multiple recessions and a pandemic. Other nations, without global reserve currency status, do not have this same opportunity to run deficits similar to ours, thereby limiting their fiscal flexibility. The United States has been in the proverbial economic catbird seat. Until now.

If the dollar’s status as the global currency reserve diminishes, there will be less demand globally for dollar denominated securities. Interest rates will therefore need to be higher to attract U.S. bonds buyers, which are necessary to finance our massive deficit. As stated by authors Tenegauzer, Vellis and Yu in BNY Mellon’s oft-cited September 2020 Aerial View Magazine

“By the end of the decade, the CBO projects US debt held by the public to exceed $33 trillion, more than 108% of GDP. Issuing so much new public debt and the Fed role in absorbing the issuance, undermines the attractiveness of the USD, especially if inflation erodes the value of the currency significantly and threatens the credibility of the Fed itself.”

This scenario – a Chinese-lead regression away from U.S. Treasury Bills and Notes, together with “bad actors” looking to avoid sanctions, and persistent inflation – would prompt increased selling of dollar denominated securities and less demand at the same time. These factors may create an environment of higher interest rates well beyond the expected pullback the Fed and market participants expect after 2023.

While the digital yuan and Petroyuans are in the early stages, they will grow as China strategically utilizes its vast economic influence throughout the world. Coupled with rising and pervasive inflation, and the fallout from the war in Ukraine – both supply chain concerns and non-Western aligned governments looking to bypass sanctions – the global dominance of the dollar is in peril. And investors should be aware that a potentially dangerous result of these forces would be sustained higher interest rates in the United States.

Wealthplicity Recent Posts