Stock Buybacks – What They Do and What Can Impact Them

Hertz announces a $2 billion stock buyback and the stock rallies 6% in one day. Should investors take this as a sign of financial strength and buy along? Or are these corporate repurchases of stock really financial maneuvering to improve income and balance sheet metrics? Or does it matter either way? As buybacks have become increasingly popular, investors need to be aware of what they actually accomplish and their outlook for the future.

After understandably disappearing last year as pandemic created numerous fiscal uncertainties for many companies, corporate buybacks have returned with a vengeance, looking to surpass the $223 billion quarterly record in the third quarter of 2021.

While these share repurchases – where corporations buy their own shares in the marketplace – became popular after regulatory changes in 1982, the current zero-interest rate, low growth environment has spurred greater utilization. Investors should understand the benefits for shareholders, management, and the overall market this surge has created.

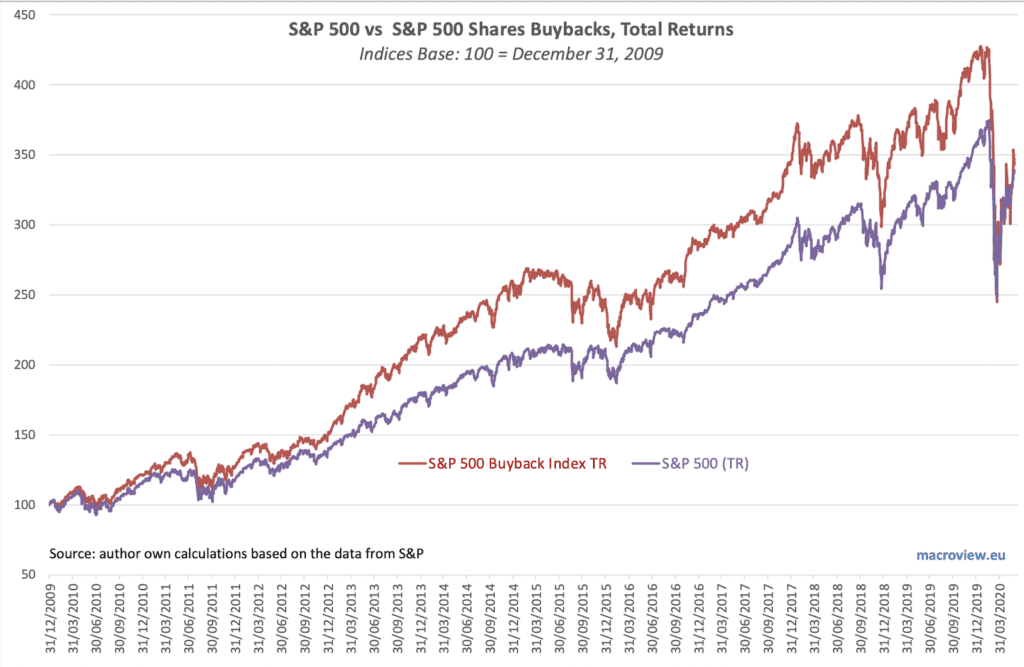

As seen in the chart above, corporate buyback strength – or the lack thereof – has helped determine the market’s direction and the magnitude of its moves. Therefore, it is important for investors to understand the benefits this surge has created for shareholders, management.

There are a number of benefits to shareholders of corporate repurchases of company stock in the marketplace:

The added demand by corporate buybacks usually provides a floor for the stock price. While the company may not be in the market every day, most institutional trading desks are aware of the desired price levels where the company will step in and buy. This will provide support for as long as the buyback is in force. As shares purchased by a company (termed treasury stock and held internally by the company and sometimes used for executive compensation purposes) removes them from the outstanding shares available, certain financial metrics and fundamentals are improved, most importantly earnings per share (EPS).

EPS is utilized universally by stock analysts as the base measure to determine whether a company’s financial condition is improving or not. By reducing the number of shares outstanding, stock buybacks inherently cause EPS to rise. And by announcing their willingness to accumulate shares around the current valuation, the company is telling investors it believes its own shares are undervalued. All these improve the financial standing and provide price support for the company’s stock benefiting existing shareholders.

There also benefits for management when a company decides to utilize a share repurchase. When a corporation has excess cash, they can spend it on R&D or other capital expenditures such as technology upgrades or facility expansions. They can also acquire other businesses, increase wages, or raise dividends. Or they can buy back shares. There are a number of reasons a company will buy their shares back from the pubic:

Corporate repurchases, as opposed to some other cash expenditures, are relatively easy to start and either pause or stop. Once authorized by the board of directors, the company’s treasury department may commence buying its stock in the market following a number of trading restrictions as to daily timing, prices paid and volume. It does not have to be in the market every day and can pause their purchases whenever they desire. This provides greater fiscal and strategic flexibility for the use of excess cash.

During the COVID-19 pandemic and the following Delta variant, managements hoarded cash due to the fiscal uncertainties they faced, and still do as the Omnicron variant has evolved. And these uncertainties make stock buybacks an easy decision when faced with extra cash.

Building manufacturing plants, expanding product lines, research and development and wholesale technological upgrades are expensive and time-consuming. Their payoffs are usually long-term and may actually have negative impacts for a company if executed incorrectly. Buybacks utilize cash and immediately improve the company’s EPS. During uncertain economic times, the low-risk, pragmatic management decision will usually be to repurchase shares.

The less shares available for trading, the less likely a hostile takeover of a company. Due to the fewer shares outstanding, it becomes more expensive for a corporate raider to acquire enough shares to force a deal. Stock Buybacks can also protect management from being ousted or from dismantling the company. And as most public companies compensate their senior executives with stock options, buybacks both support the stock and improve the financial metrics that analysts use to recommend those shares, boosting demand. Buybacks appear to be a win-win for both shareholders and management.

However, while stock buybacks have been on an upward trajectory in recent years (excluding the 2020 pandemic), they face a couple of headwinds: government policy and market valuation. The Biden administration has signed into law one bill focusing on rebuilding the nation’s physical infrastructure and sustainable energy platforms. And some form of the social services oriented “Build Back Better” will probably be passed sometime in 2022.

These government policies may create two obstacles for corporate repurchases. The first will be a refocus on capital expenditures as companies increase spending to provide the materials and services to rebuild the roads, bridges, broadband and energy sources. This will reduce the cash available for stock buybacks. The other disincentive are the increased and potential taxes.

The inevitable increase on corporate taxes will also reduce the excess cash available for buybacks. Also, there is a proposed excise tax buybacks in the social bill. While not expected to be in the final version, there are escalated discussions by policymakers to target corporate buybacks directly to help fund the massive increase in government spending.

Some believe the easy strategic decision by corporations outlined previously shifts management emphasis upon short-term stock price gains instead of long-term investments and expansion. According to Strategas Research Partners head of policy research Dan Clifton, “if Congress is making buybacks and dividends more expensive, capex becomes a preferred alternative.”

The market itself is a problem for buybacks. As the rally has continued, the impact of these stock repurchases has diminished. With higher stock prices, the excess cash buys less shares.

At the same time, higher valuations will give pause to managements paying up for their stock and wait for more attractive entry points. Another issue in the market is that share reduction – that all important factor that raises EPS – is the least in years: only 5.4% of companies reduced share counts by at least 4%, down from 1Q21’s 5.8%, and significantly lower than 1Q2016’s 28.2% (courtesy of S&P Global).

Companies are issuing more compensation stock options than ever before, which mutes the impact of their buybacks. And lastly, the overall level of corporate repurchases are made by a concentrated group of companies, predominantly led by big technology. Only twenty companies account for over 55% of 2Q21 buybacks, with Apple constituting 13% of the total, followed by Google, Facebook, Oracle and Microsoft.

When this narrow cadre decides to reduce or pause their buybacks, whether because of stock price, increased taxes or a change in economic outlook, a key factor for price support for the overall market leaders will be removed.

In Summary

Corporate repurchases are beneficial to both shareholders and management, for individual stocks and the overall market. They provide price support, increased demand and improved financial metrics.

However, due to potential increased taxes and government oversight of buybacks, coupled with an extended market, we may be experiencing a cyclical peak. Investors should be aware of the inherent positives of corporate stock buybacks. But they must also understand how the government and market valuations dynamically affect their impact and implementation.

Wealthplicity Recent Posts