There have been numerous discussions in the media recently about the danger of excessive margin debt. Many strategists point to it as a sign of an overheated and extended stock market. While there certainly are indications of stretched valuations, we believe margin debt is not one of them. We will explain what margin debt is and any predictive value it may hold for investors.

With fixed income returns remaining at historically low levels, individual investors and institutional money managers chasing returns are forced to move further out the risk profile to achieve their desired investment returns and goals. Currently, There Is No Alternative (T.I.N.A.) to stocks. And one tool available to qualified individual investors to increase returns is margin debt.

Leverage is the use of an existing asset or revenue stream as collateral to borrow funds. Similar to a home buyer using their savings and earnings track record as leverage to obtain a mortgage, margin is a loan by a brokerage firm that increases an investor’s purchasing power.

Like a mortgage, an investor must apply for a margin account. The applicant’s annual income, net worth and credit history are all considerations for approval. Once approved, there are certain restrictions and requirements that must be met to maintain the margin account:

For example, a qualified investor deposits $10,000 in cash or securities into a margin account. That allows him to purchase up to $20,000 worth of a stock: $10,000 of their own money and $10,000 in a loan from the broker. The investor’s equity in the account is $10,000.

The total value in the account must therefore remain above $12,500 in order to avoid a margin call. If a margin call does occur, the investor must deposit additional funds to bring the value of the account back to the 25% minimum or the broker will sell stock in the account in order bring the account to the necessary level.

Margin calls are painful as they usually happen during a declining market, forcing an investor to sell into falling prices.

The advantages and disadvantages of margin are similar to any use of leverage to purchase an asset. As long as the asset retains or increases in value, the leverage was neutral or productive. The borrower reaps the benefit of the increase in value above their borrowing level.

When buying a home, the purchaser builds equity when the value of their home appreciates beyond their mortgage. The negative side to leverage occurs when the asset declines in value. A home buyer can be “underwater” when their mortgage amount is more than the value of their home. This can lead to a loss of capital or possible foreclosure.

In stocks, the use of margin enables investors to increase their purchasing power, which boosts their returns. Using the prior example, if an investor bought $20,000 worth of stock using $10,000 in margin debt, and the stock doubled to a $40,000 value, the return would be 200% ($40,000 total value minus $10,000 margin debt and minus $10,000 initial investment equals $20,000 net profit; $20,000 gain divided by $10,000 investment equals 200%). Without the benefit of margin in a cash account, the initial $10,000 outlay would double to $20,000 gain, giving a return of 100%. Thus, generally, margin accounts can dramatically boost investor returns during rising markets.

However, in falling markets margin can exacerbate losses. In the prior example, if the stock purchased with $20,000 declines to $10,000 in value, the brokerage firm will initiate a margin call, asking the investor to deposit $2500 to bring the minimum equity requirement back to 25%. If the investor can not provide those additional funds, the firm will sell stock in the account until that minimum is met. This creates added selling pressure to an already declining stock.

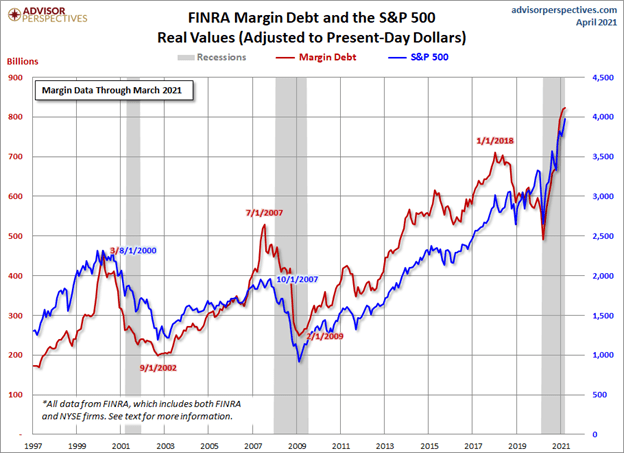

The latest data released by FINRA – the agency that monitors brokerage firms – has overall margin debt at record levels. Many pundits point to this as an indicator of unsustainable speculation.

While margin debt certainly tracks the market, rising and falling in tandem, its level is more a factor of the overall price action than a cause. It is the rising or falling values of stocks in margin accounts that provides investors with greater or lesser purchasing power. It is the byproduct of the market, whether bull or bear. Therefore, record levels in margin debt are coincident with record levels in the stock market and are not a harbinger of doom.

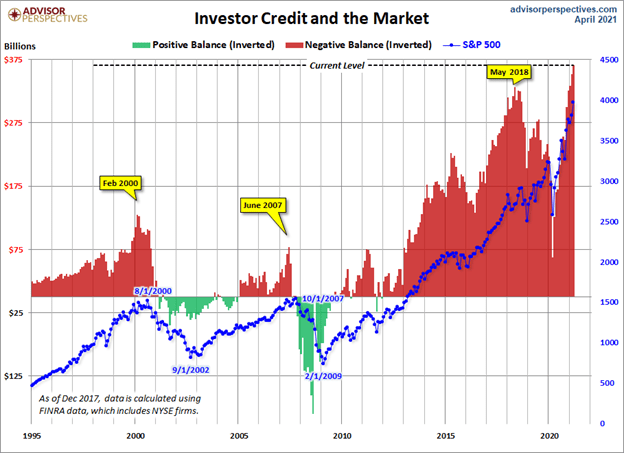

However, there is one component related to margin that is worth notice. That is the trend in margin credit. In margin accounts, investors pay interest on the amount borrowed from the brokerage firm.

That is the debt. Unused funds in the account – the amount of equity in the account in cash – receives a credit, similar to a savings account at a bank. The key is to observe for a trend change.

An increase in the amount of credit would be indicate that the overall number of margin accounts are not taking advantage of their total purchasing power, signaling a reluctance to be fully invested. Conversely, a trend change from declining credit would indicate that individual investors are more confident in the market.

In Summary

Margin is an investment tool that allows investors to increase their purchasing power in order to maximize their returns. However, as with all investment components, there is risk. Margin calls will limit liquidity or magnify market losses. Margin accounts are not for everyone, and individual investors need to be fully educated about the advantages and disadvantages beforehand. And its level is just an indication of the direction of the market. While there are signs of extended valuations, margin debt is not one.

Wealthplicity Recent Posts