Special-purpose acquisition companies (SPAC) have raised more money – over $38 billion – than traditional IPOs, with over 130 going public so far in 2021 and many more in the pipeline. While these “blank check” companies have been around for decades, their current surge in popularity may be signaling an over-heated equity market.

A SPAC is a public company that exists only to purchase or merge with a private business. During this reverse merger, the stockholders of the target company become the majority shareholders of the new company. The formerly private company becomes the publicly traded entity. This bypasses the traditional IPO process.

SPACs provide quicker access to financial market funding. They are usually less equity dilutive for the target company management than private equity sources. SPACs are also led by talented and experienced management teams with proven track records of growing businesses. And Unprofitable yet potentially disruptive companies may utilize a SPAC versus the more fiscally rigorous IPO process. Thus, SPACs enable a private company faster and more efficient access to the market.

SPACs are usually structured with a two-year life. If the SPAC management team does not identify or close a deal with a target company within two years, the firm does a “De-SPAC” transaction and all funds are returned to the investors. As SPACs are created solely to make a deal within a limited time period, the management may overpay for a company, rush too quickly to make a deal, or target an unprofitable risky business that is not “public company ready” due to a lack of internal controls. These deals may lead to litigation, reduced share prices or even SPAC investor redemptions, with the company returning the investors their money.

The current SPAC environment.

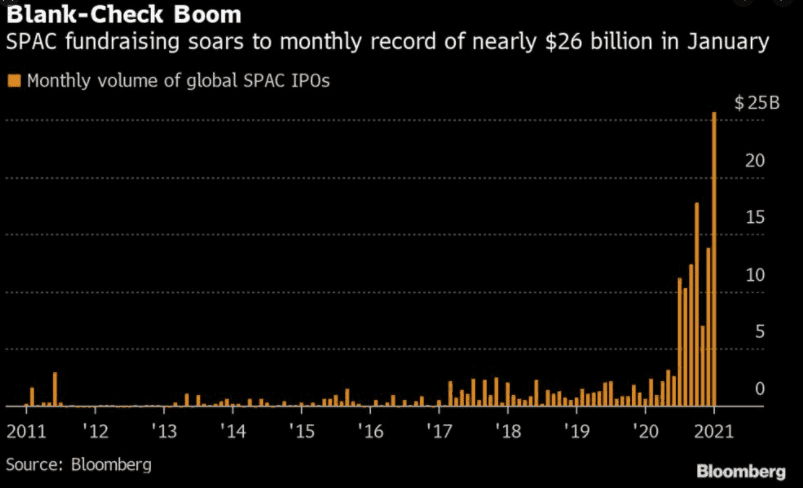

The record month in January of 2021 of SPAC listings is fueling the busiest start ever of initial public offerings. The over $60 billion of funding globally is over five times last year’s initial levels as companies have accelerated coming to the market to satisfy professional money managers’ need for outperformance. The current low-interest rates-forever narrative has forced these institutional portfolios to chase anything that may provide out-sized returns. And the IPO market – and now SPACs – are some of the most readily available investment vehicles that may produce such returns.

In Summary

Market tops may be made by market-external factors, such as war, or market-internal factors. These internal indicators are basically over-valuation plus rampant speculation. The Standard and Poor’s 500 Stock Index is currently trading at a Price-to-Earnings Ratio (the price of the index divided by the average of the aggregate earnings per share of the 500 underlying stocks in the index) over 35 times. The P/E Ratio is a widely accepted measure of relative valuation of a stock or index over a specific time period.

The current value is well over the historical modern-era average of approximately 20 times, going back to 1950. And the recent surge in Bitcoin, the social media driven spike in GME and this SPAC-led surge in a multitude of companies coming to market are all great examples of over-speculation by professional and retail investors alike.

No one can predict specific market tops or bottoms. However, the current speculative frenzy demonstrated by this record-breaking demands for SPACs – among other indicators – should signal investors to at least re-evaluate their near-term risk profiles.

Wealthplicity Recent Posts